A Better Question than Active vs. Passive

Over the last few years, the active vs. passive debate has been beat to death. The argument stems around whether it is worth your money to invest in an active manager to “beat the market”. While the active camp would obviously argue yes, the passive camp has plenty of evidence to demonstrate that it is quite difficult to find a manager who can consistently outperform his or her benchmark, year over year. In this post I would like to put a different frame around the conversation by briefly covering the following points:

- The merits and hurdles of active.

- Defining and redefining passive.

- Providing a better question for investors to ask themselves, rather than simply “active or passive?”

ACTIVE INVESTING

The universe of active management takes many shapes. Most conventionally, retail investors would recognize a mutual fund as an active manager. But in addition to a mutual fund, an active vehicle can take on many forms – hedge funds, private equity funds, limited partnerships, and actively managed ETFs, to name a few. When you choose to be an active investor, you are are entrusting a capital allocator to make discretionary decisions on your behalf. To sell sell MSFT, buy AAPL, go long orange juice futures, etc. Buffett, Lynch, Gross, and Soros – to name only a few – provide an argument for entrusting and paying for a pro. The issues is, there’s a reason why you likely know at least a couple of those names…because there can only be so many. If it were so easy, we would all be active managers and these guys would hardly stand out. The other side of the coin is the mountain of evidence that, by and large, active managers do not provide alpha over the long run. There are lots of reasons for this, most notably there is the persistent burden of transaction costs and tax liabilities. Beyond those inherent hurdles, active managers are not charitable entities. They require compensation along with their teams of analysts, traders, compliance officers, and in-office baristas. So even if you prove to make wise investment decisions as a money manager, you have to compensate for the cost of doing business as well as your ongoing tax burdens in order to even match the performance of a passive index.

Now is this all to say active managers are worthless? Certainly not. First of all, active managers are doing the heavy lifting. They perform due diligence and price discovery – two functions that benefit the rest of us. On top of that, there will always be investors who prefer the peace of mind knowing that they have professionals putting their capital to work. And they may gladly give up market returns for that sense of security. As a thought exercise – if you had to put all your assets into one vehicle today, for the rest of your life, who or what vehicle would you choose? Personally, I would pause before picking the passive index fund.

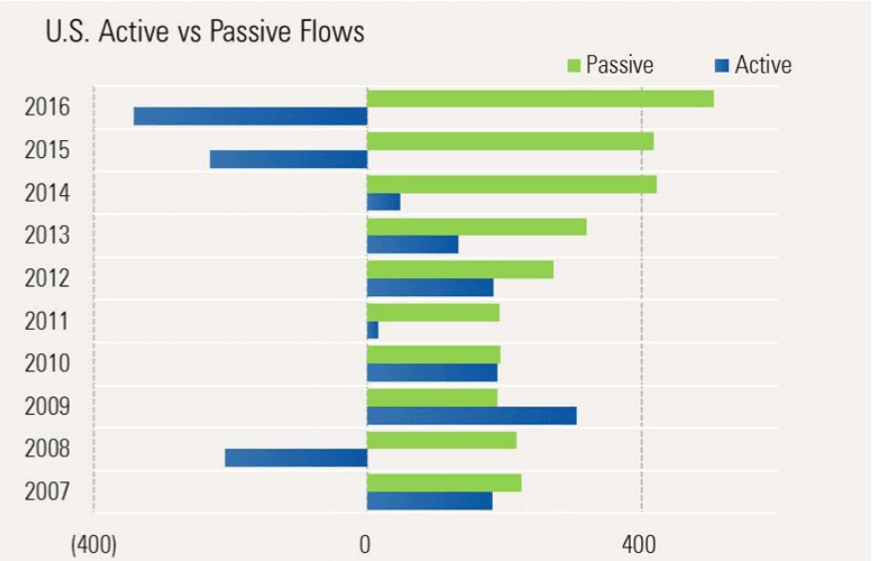

Active managers have had a rough go of it. Take, for example, Morningstar’s comparison of asset flows into passive vs. active vehicles over the last 10 years:

Vanguard, the poster-boy-turned-poster-monster for the passive world, has grown from $1 trillion in AUM to over $4.2 trillion in the last seven years. Trillion, with a “T”. Seven, with a “holy cow”. That’s growth of $1.2 billion a day. A chunk of that increase is attributed to increased asset prices, but the point stands. While I don’t think we’re witnessing the death of the active manager, there are major shifts and challenges afoot.

PASSIVE INVESTING

If active management is Ben and Jerry’s Chunky Monkey, passive investing is fat-free vanilla custard. Instead of entrusting an active professional team to manage assets, you are investing your capital across the broad universe of whatever asset class it is you wish to invest in. The S&P 500, the MSCI All World Cap Index, US Treasury Bonds, etc. The traditional vehicle is an indexed mutual fund or ETF. You are accepting the market return, and no better. And you accept the price volatility that comes with that asset class. The upside is a tax-efficient, low-fee investment vehicle. No portfolio manager to pay means more higher returns, all else being equal. And the evidence – at least for most major asset classes – tells us this is a prudent choice.

But in this simplistic debate, there is a major point missing, which is: a passive investment vehicle does not equal a passive investor. The only passive investor – as I see it – is the investor that allocates her capital to a basket of all securities across the globe, weighting each asset class according to it’s relative size to the overall investable global portfolio. Through economic cycles that portfolio may contain vastly different weights in stocks, bonds, commodities, real estate and so on. The passive investor accepts that fluidity and remains invested at all times. Is this possible? Off hand I don’t know of a product that offers such exposure. It’s likely possible to closely mirror with the use of ETFs. Whether it’s useful is another question and conversation. Absent that approach, the rest of us are active investors, and “buy into” to some extent the merits of active investing. An investor who decides to shift his portfolio from 60/40 to 40/60 is being active. An advisor who provides value-add by regularly rebalancing client portfolios is being active, as is the advisor who decides to shorten the duration of a bond portfolio. Robo-advisors are active as well.

WHAT’S BETTER THAN PASSIVE AND ACTIVE?

So rather wondering if you’re a disciple of passive or of active, I propose you ask yourself a better question: what is a long-term plan that I can stick to? This question may seem easy today – at some stage of a multi-year bull market with historically low volatility – but it will absolutely challenge investors at the next prolonged turn down. I don’t have a crystal ball, but I would wager that a chunk of “passive investors” will run for the hills when the worm turns. Another chunk will login to their robo platforms and scale back their risk tolerance from aggressive to moderate. That is no better than the guy who continues to chase the “next Buffett”.

The idea of a plan helps me wrap my head around the best approach for my clients. As a human, I too am susceptible to feeling fear and running from volatility. I too read headlines and feel the fight or flight instinct we all carry in our DNA. The better approach is to develop a philosophy, a methodology, and stick to a rules-based investing approach that is supported by historical evidence. Turn off the TV, remove (or at least reduce) the emotional temptations, and invest for the long run.

So – what’s your philosophy?

LAYLINE ADVISORS, LLC (“LAYLINE ADVISORS”) is a registered investment adviser offering advisory services in the States of New York and Texas and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, LAYLINE ADVISORS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement and suitability for a particular purpose. LAYLINE ADVISORS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall LAYLINE ADVISORS be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if LAYLINE ADVISORS or a LAYLINE ADVISORS authorized representative has been advised of the possibility of such damages. In no event shall LAYLINE ADVISORS, LLC have any liability to you for damages, losses and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.