An Opportunity Abroad?

As of mid-March, we’re just under 2% off the US broad market’s all time high. The equity market has rallied at a staggering rate since Republicans took control of the federal government in anticipation of deregulation, comprehensive tax reform, infrastructure spending, and in general a pro-corporate era. The issue is this all relies on the if-come our notoriously dysfunctional federal government can actually accomplish such goals. Take, for example, the newly proposed health care reform. Not a day after Speaker Ryan introduced the bill were fellow Republics going to the press to lament it. Should we continue to see continued or worsening pushback and infighting, the time line for other stimulative measures gets delayed at best.

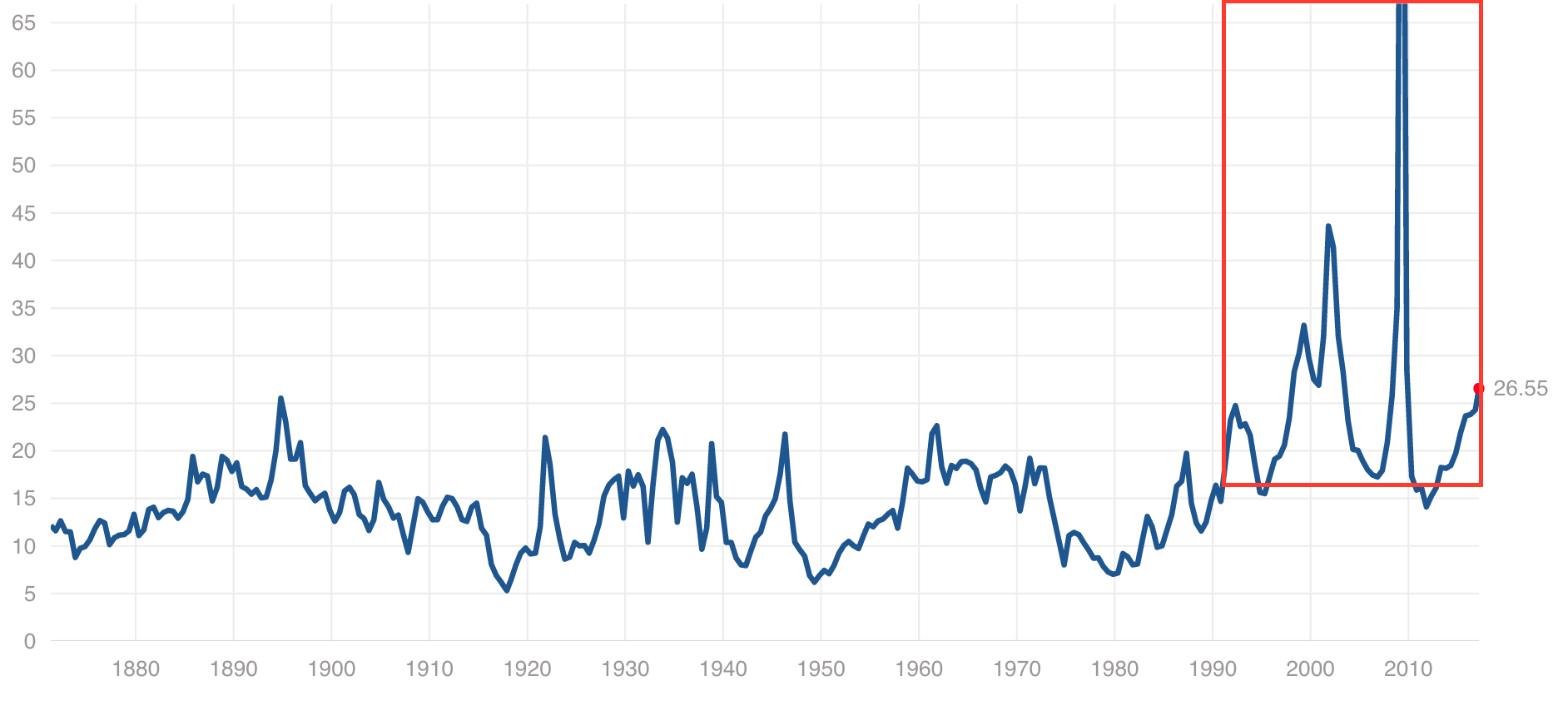

So that brings us to the US market and the merits of its current valuation. These days one is hard pressed to spin the market as cheap or even moderately valued. The CAPE ratio currently sits at 29.14 and the trailing 12 month PE at 26.55. Both are well above the mean values of 16.73 and 15.64, respectively. That said, valuation is a notoriously bad timing tool. It provides us context, but by no means an answer. Markets can remain expensive for periods of time before they correct. For example, if you used the CAPE ratio to determine the market was “too pricey” and sold any time it sat above the historical mean, you would have stayed on the sidelines from the mid 1990s until today:

The argument for a “new normal” with elevated value metrics has been made. And there’s certainly merit. It’s a much deeper topic than I can reasonably cover – from technological changes, to changes in corporate capital structures, and the globalization of securities markets. One prevailing argument – that I do want to mention – is the current interest rate environment. As central banks and other market forces drove rates to zero, investors were pushed into risky assets in search for yield. Eight years into the bull market, with US stocks at high valuations, this dynamic remains central to the question – what to do? Those same investors are now faced with remaining in frothy stocks or reallocating to those modestly yielding bonds. At nominal rate of ~2.6% for example, the 10 year US Treasury bond does not offer a relatively attractive opportunity. At say 5%, on the other hand, one may be quicker to move out of an expensive stock in order to receive a historically decent yield with much lower volatility. The other salient point is that UST bondholders will get hammered should longer rates increase materially. And that is a feasible scenario should US growth continue to chug along.

To recap, I have touched on two asset classes – expensive US stocks, and unattractive US government bonds. The other option is to hide in cash, but that is seldom the answer for a long term answer. Over the long run inflation can substantially erode the buying power of the dollars you stuff in your yoga mat.

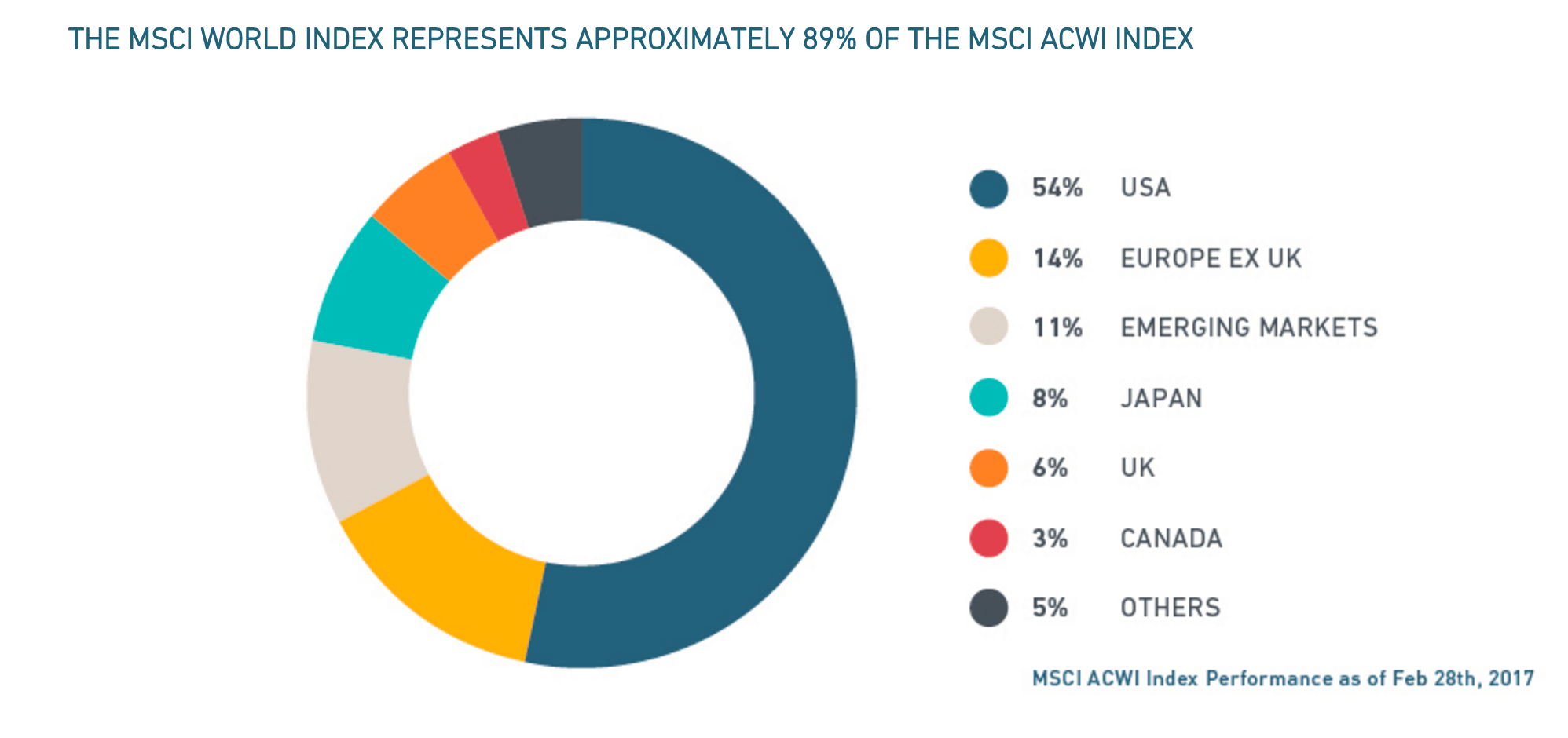

One strategy I believe warrants a serious look – especially for longer term investors – is to take this opportunity to rebalance into a diversified basket of more cheaply valued countries. And why not? There is no shortage of selection, as equities outside the US now account for approximately 46%, according to the MSCI World Index:

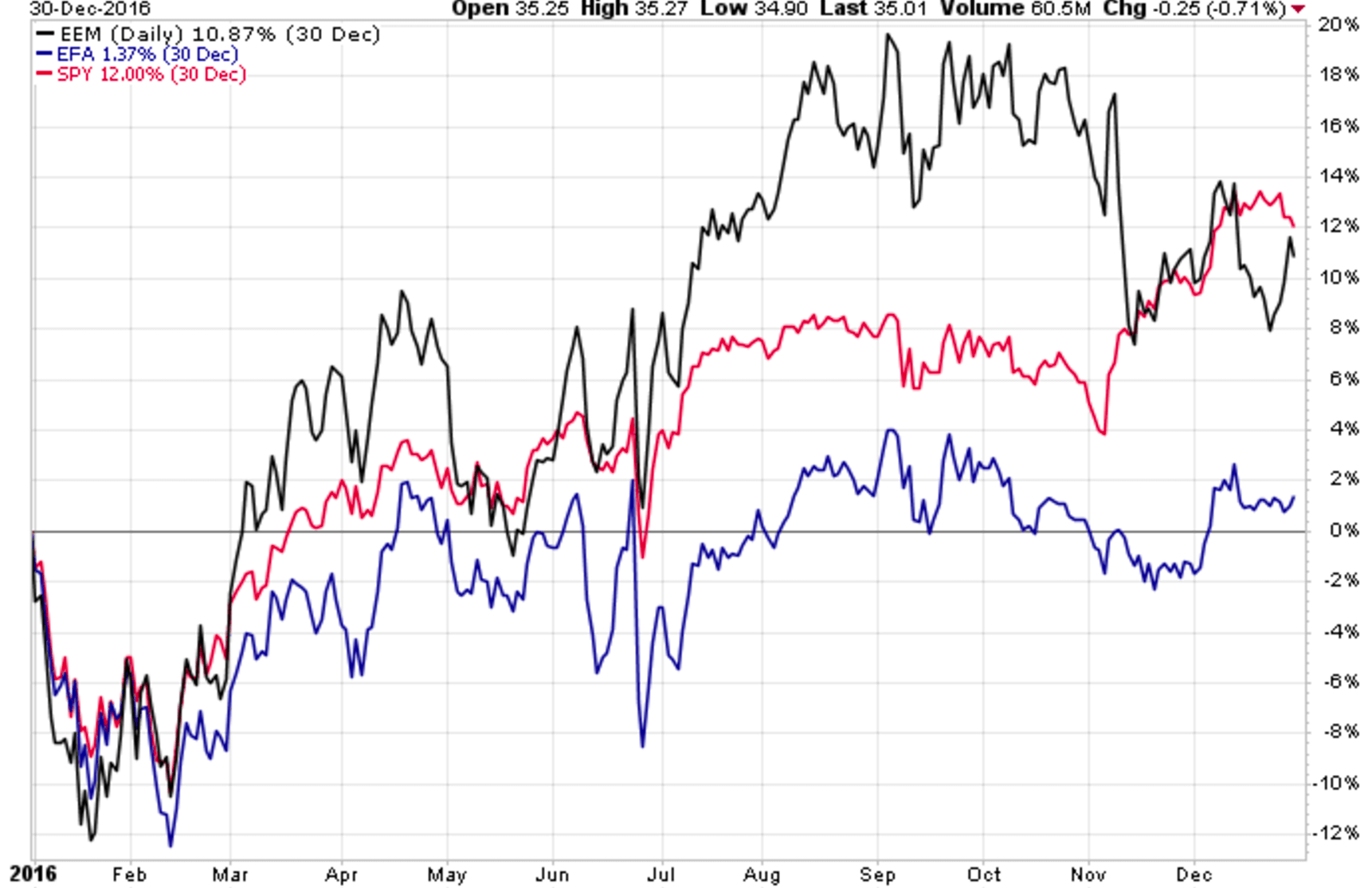

Yet at the same time, as Vanguard reported in 2014, the average US mutual fund investor only held 27% of their quiet allocation in non-US funds. 27% of their equity allocation. For the typical 60/40 investor that’s 16.2%. This phenomenon is called home country bias. Americans, Canadians, Japanese, Swedes – we all tend to overstuff our portfolios with what we think we know. Another objection is the idea that there’s “too much geopolitical risk” right now to go abroad. To that, I ask you to imagine the following…we turn back time and are back in January 2016. But somehow you retain knowledge of all the headline events of 2016. You know about the impending Chinese growth scare, Brexit, Zika outbreak, the impeachment of Brazil’s president, and the election of Donald Trump, to name a few fun ones. What would you think about investing globally? Would you be encouraged by the future environment, or have reservations? In fact, all three major global equity baskets posted positive 2016s:

OK so maybe we can agree we can’t know the future. And even if we did, perhaps that information wouldn’t be of any good use. What are we to do? Again, let’s take a look the current opportunity set to identify attractively valued regions.

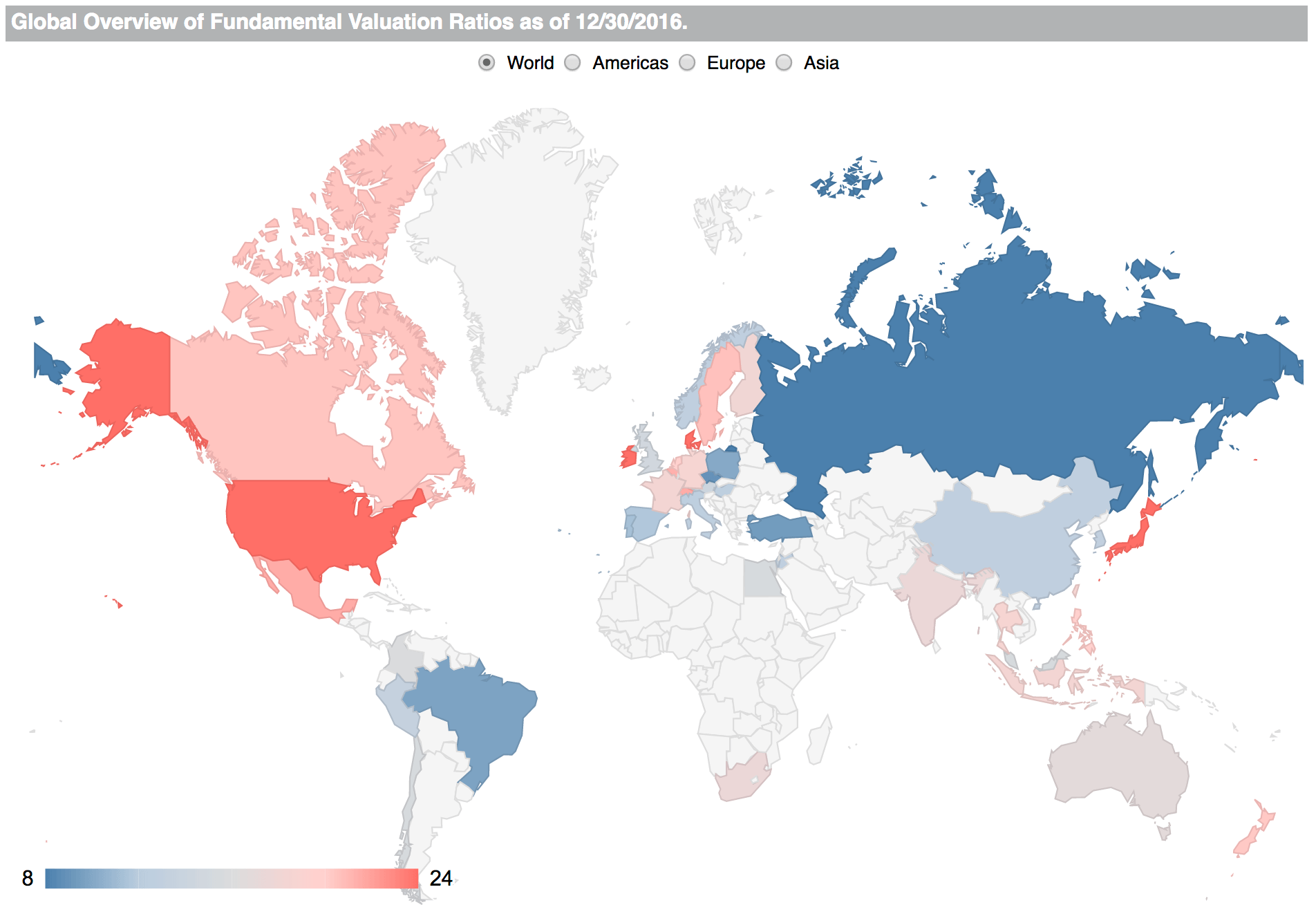

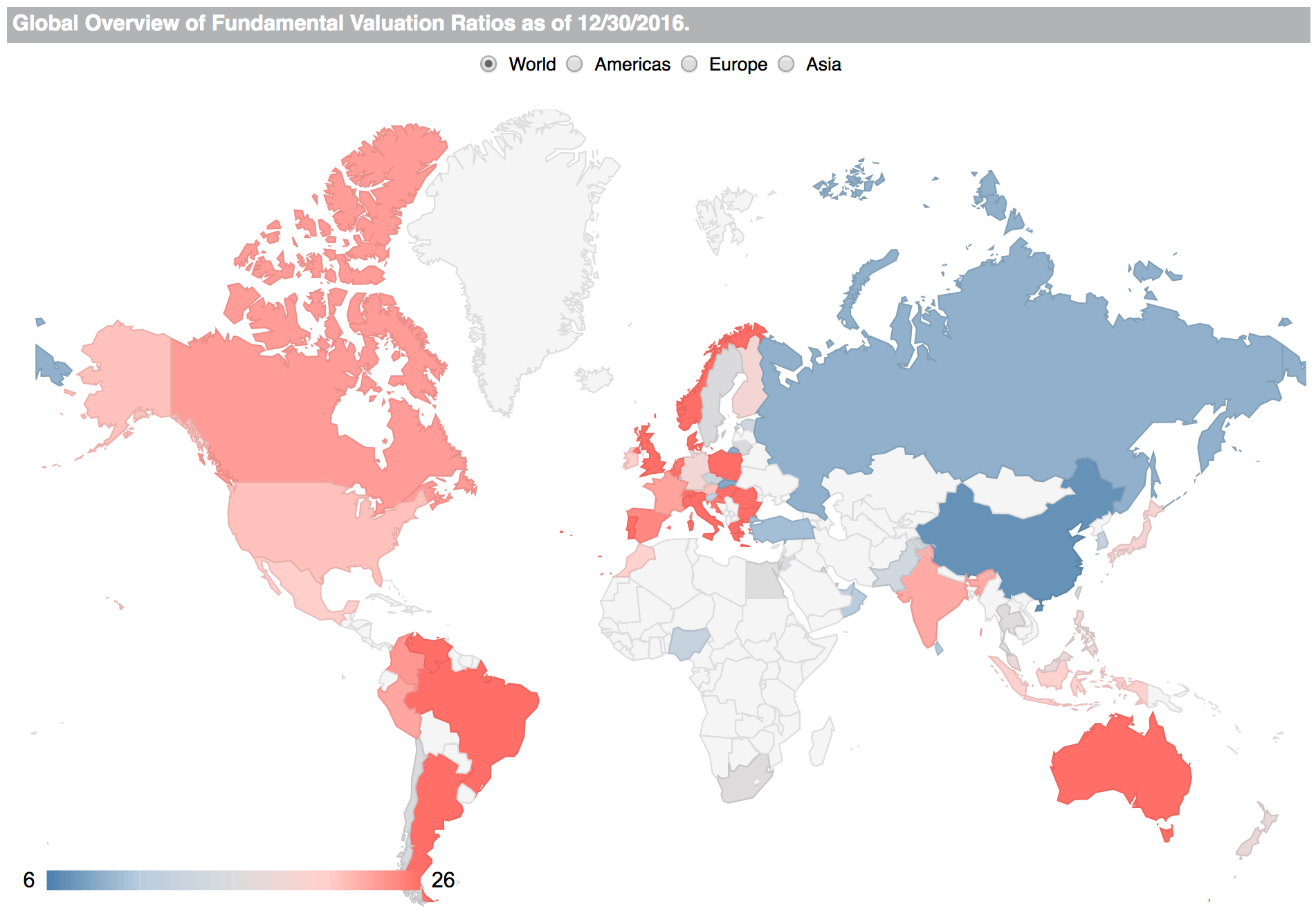

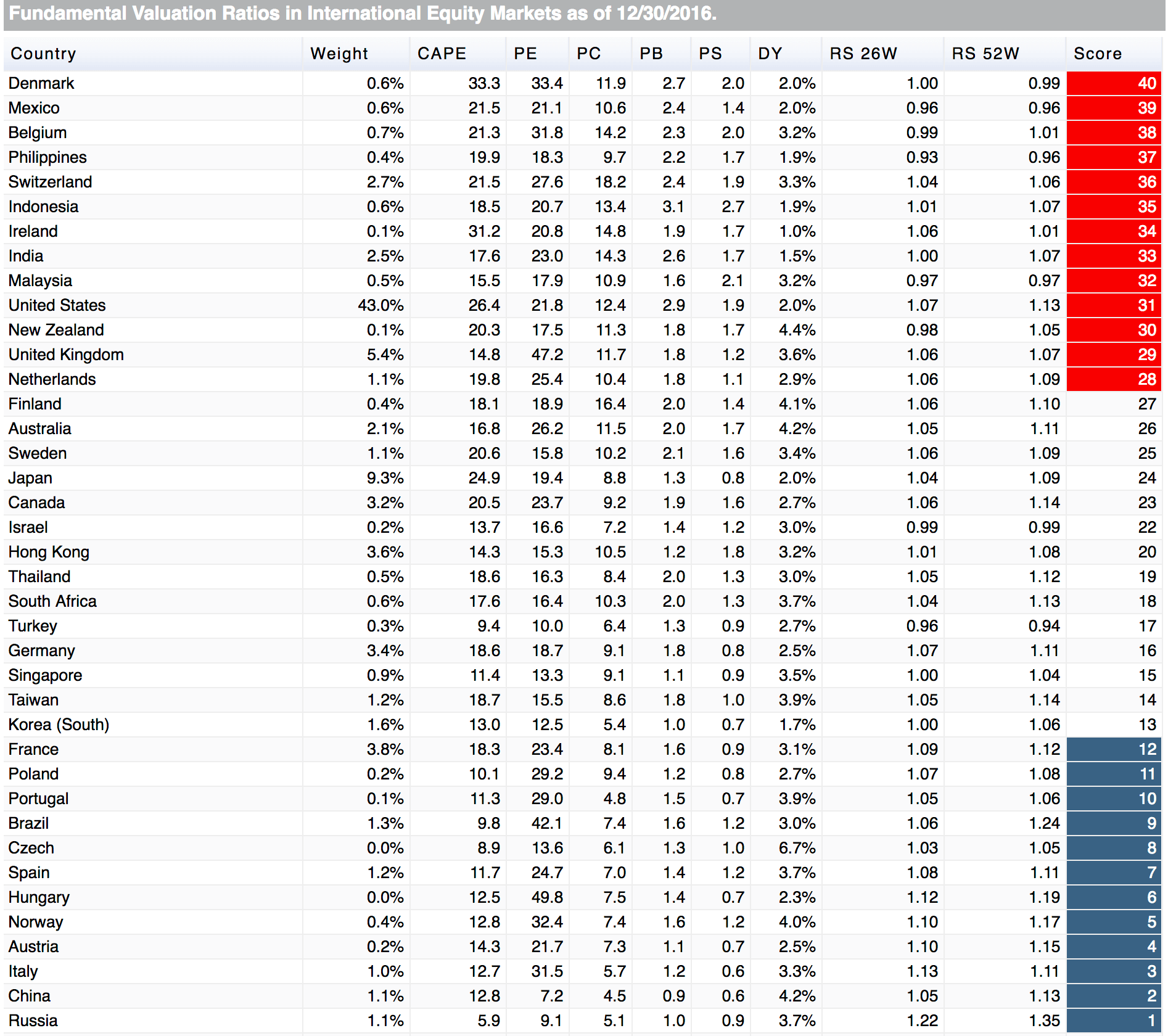

Below are two maps from Star Capital site. The first, world country rankings for cheapness as measured by the CAPE ratio:

And second, the same idea, but using the trailing 12 month PE:

Finally a composite ranking of all measured countries (most expensive to least expensive):

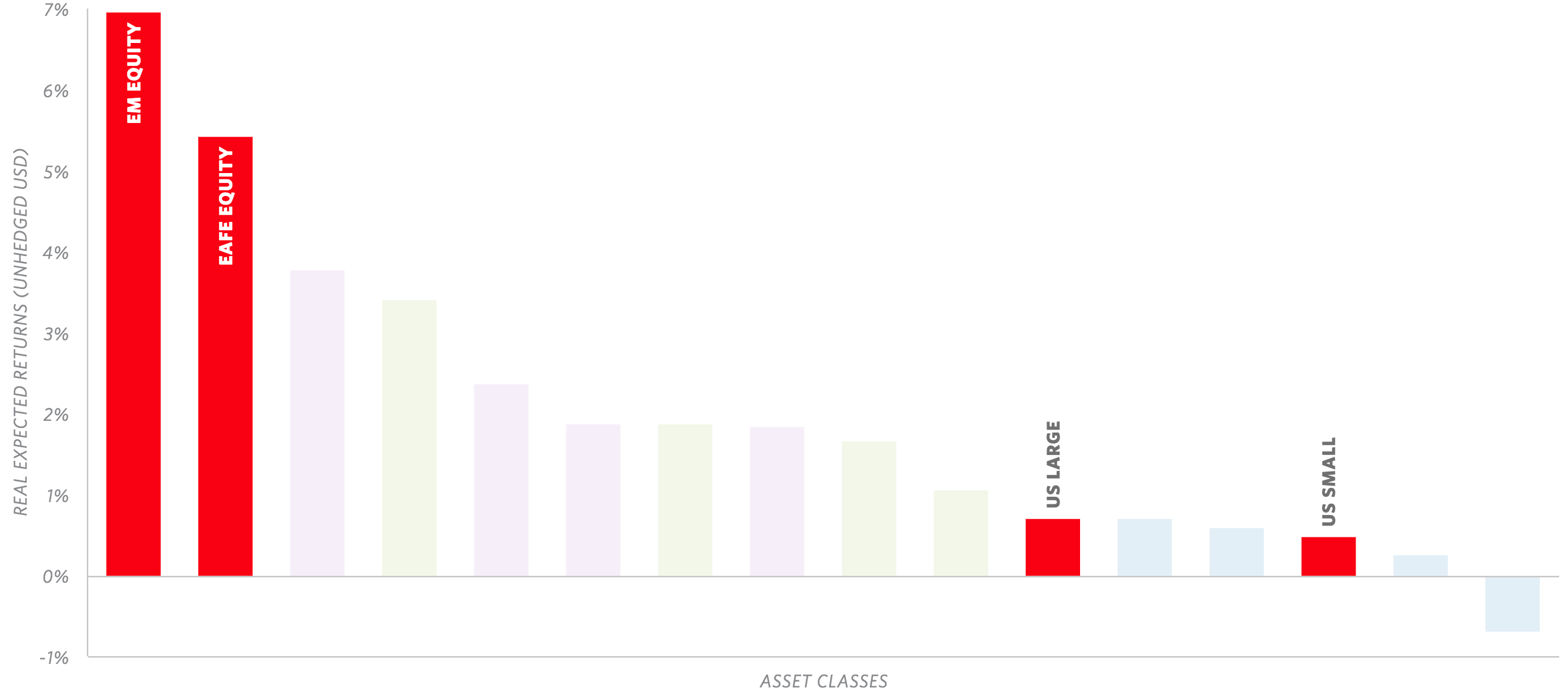

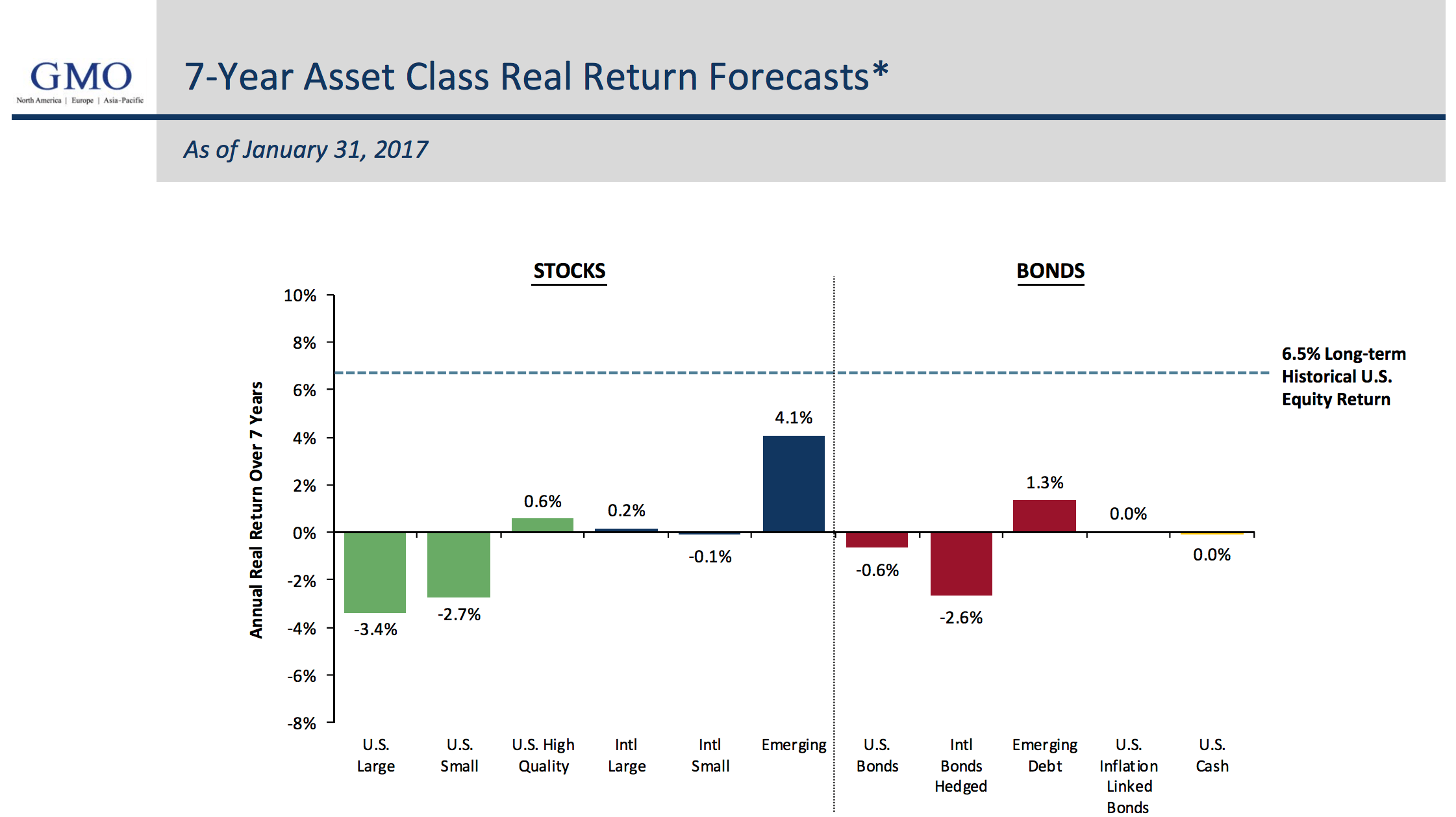

Depending on your tool of choice, there is value to be found in parts of emerging Europe and EM. Recall that at the beginning of this post the issue at hand was what to do with US centric portfolios that now look expensive. All else equal, long term investors can expect better results from cheaply valued securities, and that is the opportunity EM and parts of Europe are handing us. Research Affiliates acknowledges this in their 10 year expected returns chart:

It cannot be stressed enough, this is in the context of a long term goal. No one can predict year to year which regions will perform well and which won’t. There may be years of negative performance across the board. I’m sure there are currently lots of US investors that have given up on internationals. But that is also what creates dislocation and opportunity.

To summarize:

- US stocks have hand a tremendous run.

- While they could continue, it’s no secret they’re expensive.

- Bonds aren’t much more attractive, offering unattractive yields and interest rate risk.

- International stocks currently sit at more attractive valuations.

- All else equal, a cheaper valued security should deliver stronger performance over the long run.

LAYLINE ADVISORS, LLC (“LAYLINE ADVISORS”) is a registered investment adviser offering advisory services in the States of New York and Texas and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, LAYLINE ADVISORS disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement and suitability for a particular purpose. LAYLINE ADVISORS does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall LAYLINE ADVISORS be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if LAYLINE ADVISORS or a LAYLINE ADVISORS authorized representative has been advised of the possibility of such damages. In no event shall LAYLINE ADVISORS, LLC have any liability to you for damages, losses and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.